University of Wisconsin Center for Cooperatives

Research on the Economic Impact of Cooperatives

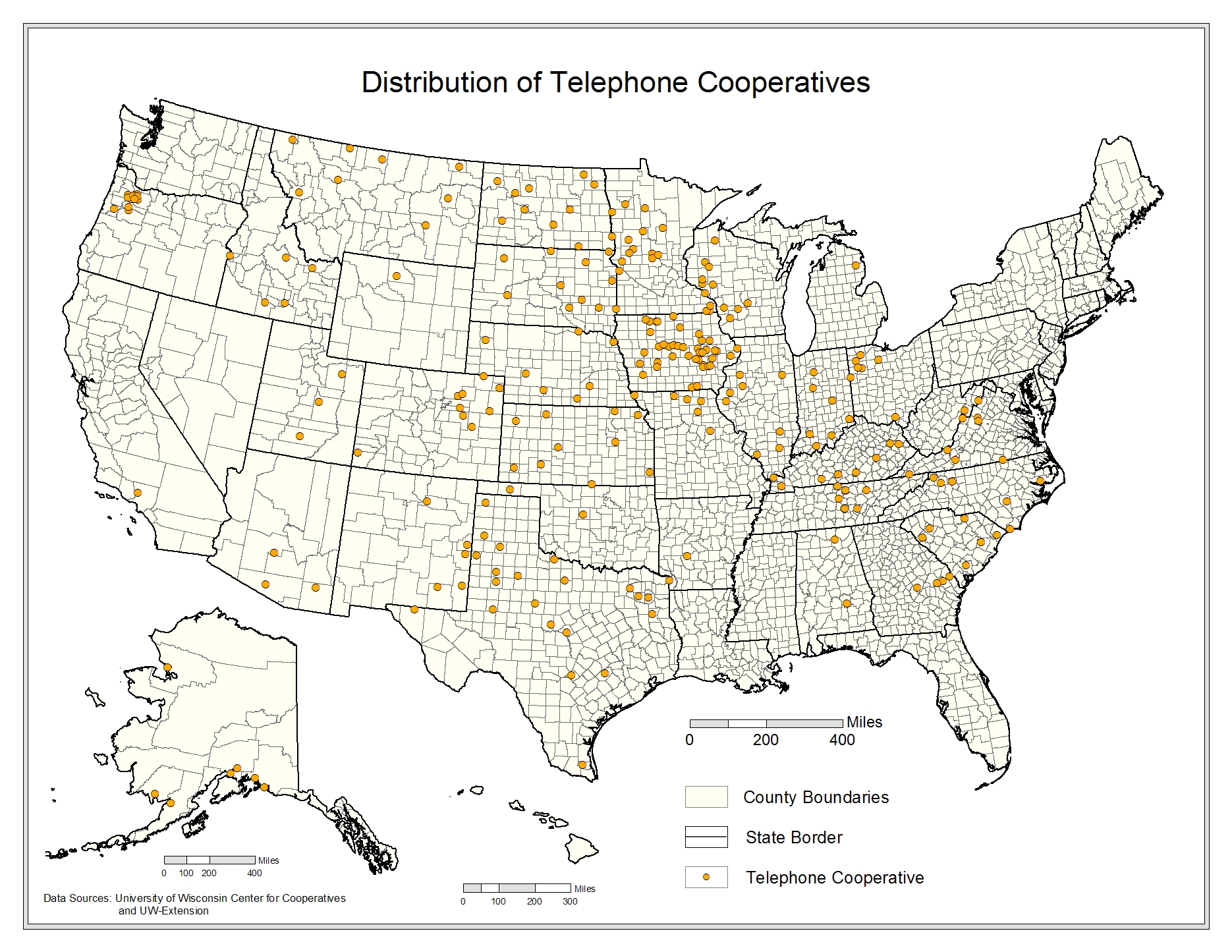

Rural Telephone Cooperatives

Overview

The 260 U.S. telephone cooperatives are consumer-owned utilities established to provide quality telecommunications service at reasonable cost. They offer various telecommunication services to 1.2 million rural Americans in 31 states. Telephone cooperatives are most often located in rural areas where there is a strong cooperative tradition. They provide local telephone exchange services, long distance telephone operations, direct broadcast satellite, wireless, TV, mobile radios, cellular and key systems, and Internet access.

While size varies significantly, the average telephone cooperative has >5,000 subscribers, 31 employees, and an annual revenue base between $1-5M. Like their rural electric counterparts, telephone cooperatives serve a very small proportion of the nation's telephone subscribers - about 5% - but their service area covers >40% of the country’s land mass (National Telecommunications Cooperative Association [NTCA](a)).

History

The lack of telephone service in rural areas spurred the development of small telephone companies, and in areas where farmers were already familiar with agricultural cooperatives, the model was often used to provide telephone service to their communities. Although nearly 6,000 cooperatives, mutuals and other types of companies were providing telephone service to rural consumers by 1927 (NTCA)(b)), poor business practices caused many to fail, leaving farmers and rural residents with significantly fewer telephones in 1940 than in 1920 (Hatfield, 1994).

Major changes came to rural telephone companies with the advent of the New Deal. The 1934 Communications Act created the Federal Communications Commission (FCC) to provide quality telephone service to all Americans at reasonable rates. However, rural telephone service availability and quality remained poor until long-term, low-interest loans for rural telephone companies became available as part of theREA loan program in 1949. In 1961, the definition of telephone service was expanded to include provision of educational television, and in 1971, the Rural Telephone Bank (RTB) was created to supplement direct loans from REA. RTB was jointly owned by the Federal government and rural telephone companies, including cooperatives, until 2008, when the availability of other sources of capital made it obsolete.

Between 1934 and 1982, American Telephone and Telegraph (AT&T) dominated the entire telecommunications sector. Independent local carriers, many of which were cooperatives, provided local wiring to end users and purchased access to long distance calling from AT&T. The 1982 breakup of AT&T created the seven regional carriers known as the “Baby Bells,” but demands to completely deregulate the industry continued until passage of the Telecommunications Act of 1996. This Act was the first major overhaul of the 1934 Communication Act, and set new standards with its competition and universal service provisions.

During the 1980s, advances in wireless and satellite technology brought about a tremendous increase in demand for telecommunications services. The National Rural Telecommunications Cooperative (NRTC) was formed in 1986 to foster the development and growth of satellite technology in rural America. NRTC is a joint venture of the NRECA and the CFC, with support from the NTCA. Members include both locally owned commercial telephone companies and cooperatives.

Industry Niche

The telecommunications industry provides businesses, government, and retail consumers with a wide variety of communications products, including voice communications, internet access, data, graphics, television, and video. These products are provided through fixed wire lines and wireless systems. While wire line communication service continues to be dominant, new wireless communications technologies, internet services, and cable and satellite program distribution are fast gaining an equal share of the industry. The industry is characterized by substantial and fast-paced change in structure, technology, customer preferences, and government regulations, and is dominated by very large investor-owned firms.

The “telecom service value chain” combines production and sales of the “end device,” (e.g., a telephone) end-user connection to telecommunications services by wires and cables and a local carrier that maintains switching equipment that routes “content” to its final destination in the local area, or to another switching center that routes the content to its final destination. The local carrier also maintains the cable network that forms the backbone of the industry. Regional carriers are switching centers that provide content routing to and from the local carrier within a large (several-state) geographic region. The final step in the chain is long distance carriers that provide routing among the regional carriers and internationally.

While the Telecommunications Act of 1996 provided for entry of many competitors at all levels of the industry, the industry has also seen significant consolidation. AT&T has expanded back through the chain to become a local and regional carrier, as has Sprint, the other giant in the industry.

Access to bandwidth has been a critical factor in the capacity of telecommunications firms to compete effectively, given the rising volume of high-bandwidth transmissions, such as internet data. To expand and upgrade bandwidth capabilities by extending higher capacity fiber optic cable to rural customers is very expensive, however, and many rural wired carriers are leveraging DSL technologies to compete.

To support the delivery of services to rural areas in this competitive environment, telephone cooperatives receive governmental support through RUS loans, which are available for voice telephone service, broadband access, distance learning, and tele-medicine. RUS also makes loans to telephone cooperatives to facilitate third-party lending for rural economic development job creation, and provides significant technical assistance.

Another important source of funding for innovation comes from mandatory contributions made by international and interstate communications carriers to the Universal Service Fund. The fund was established by the FCC to assure that quality advanced telecommunications services are available to all consumers at equitable prices. Although determining what percentage of this amount went to telephone cooperatives is not possible, the websites of telephone cooperatives reflect the importance these cooperatives place on receipt of universal service funds.

Telephone cooperatives, and commercial telephone companies, are subject to regulation by the FCC, the Interstate Commerce Commission, state public utility commissions, and county and local regulators. In many states, however, cooperatives are not subject to state regulation because they are consumer-owned, and considered self-regulating organizations. In addition, like other RUS borrowers, telephone cooperatives are subject to regulations and guidelines established by RUS.

Organizational structure

Telephone cooperatives are incorporated under state statutes specific to telephone cooperatives, or under the state’s general cooperative or corporate laws. Telephone cooperatives are considered nonprofit corporations and are granted Federal tax-exempt status under IRC section 501(c)(12), which requires that they be a cooperative, provide telecommunications services, and meet the 85% income from members rule.

Each telephone cooperative customer is a member-owner of the cooperative. Membership is required of all customers. Although telephone cooperatives were originally monopoly providers, many residents in their service areas can now choose among several telecommunications suppliers. Any person, firm, association, corporation, or political body within the cooperative service area can become a member. Members elect a board of directors from among the membership on a one-member/one vote basis. The number of directors on the board varies, depending on the size of the cooperative. Bylaws may provide that directors be selected from specified territorial districts and may further limit voting for any director to members located in the territorial district that a director represents. Directors are not compensated for their service.

Rural telephone cooperatives strive to operate at cost. However, like other businesses, telephone cooperatives must accumulate equity capital to support their operations and new initiatives. Net earnings allocated to each member based on patronage are called “capital credits”, and the underlying value is retained by the cooperative for a period of time. Most telephone cooperatives have capital credit retirement programs in which the value of past allocated capital credits is returned to members, most frequently as a credit on their telephone bill.

Population Discovery and Data Sources

The list for rural telephone cooperatives comes from NTCA. All economic data comes from survey work undertaken by the UWCC and Guidestar. The survey response rate for rural telephone cooperatives was 39.5%, and all reporting cooperatives provided us with 2005 - 2007 fiscal year-end data. The data collection and survey methodology is discussed in detail in the Data Collection section in the Appendix.

Economic Impacts

Table 4-5 shows that we acquired data on 158 telephone cooperatives, and collectively these firms account for >$5B in assets, exceed $1.5B in sales revenue, and pay >$521M in wages. There are approximately one million memberships and 12,000 employees. As Table 4-5.2 shows, by extrapolating to the entire population (255 firms) and adding indirect and induced impacts to this activity, telephone cooperatives account for close to $3.9B in revenue, 23,000 jobs, $1.3B in wages paid, and $1.8B in valued-added income.

| Economic Impact | Multiplier | Unit | Direct | Indirect | Induced | Total | |

|---|---|---|---|---|---|---|---|

| Industry Revenues | 1.608 | million $ | 2,412 | 653 | 814 | 3,879 | |

| Total Income | 1.757 | 1,022 | 329 | 444 | 1,795 | ||

| Labor Income | 1.530 | 858 | 204 | 251 | 1,313 | ||

| Employment | 1.785 | jobs | 12,634 | 3,965 | 5,954 | 22,553 | |